Retirement investment funds plans offer an expense advantaged method for reserving cash away for retirement. On the off chance that you add to an enlisted retirement reserve funds plan (RRSP), you have the adaptability to control how you put away your cash. There are sure principles on how much you can add to your RRSP. Assuming that you figure out you’ve made a Fix RRSP Over Contribution, you should address it. You have space for error before you need to suffer a consequence. Contributions up to $2,000 of the permitted most extreme will not get you punished.

An enlisted retirement Fix FD on Boiler is a typical retirement plan that permits you the adaptability of controlling the interests in the record. You can add to your own RRSP until age 71. You can likewise add to the RRSP of a companion or precedent-based regulation accomplice until they turn 71.

The Canada Revenue Agency draws certain lines on how much a citizen can add to a RRSP. Assuming the roof is penetrated, punishments can result – and explicit moves should be initiated to determine what is going on.

Assuming that you need to make good on this 1% expense, finish up a T1-OVP, 2021 Individual Tax Return for RRSP, PRPP and SPP Excess Contributions return and send it to your assessment place. At the point when you record the return, send archives, for example, bank explanations affirming the dates of contribution(s) and withdrawal(s). Kindly note Fix RRSP Over Contribution slips don’t contain this data. Pay the expense in no less than 90 days after the schedule year try not to late-document punishments or interest charged.

What is a RRSP Over Contribution?

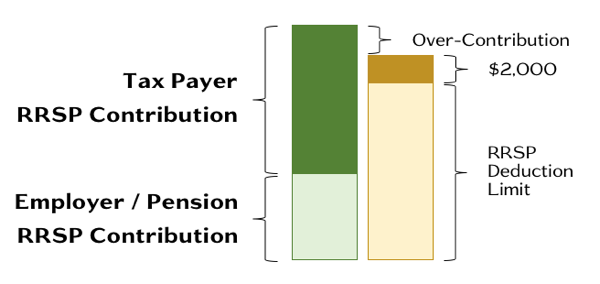

As indicated by Canadian duty regulation, anything in overabundance of your derivation limit in addition to $2,000 is viewed as a Fix RRSP Over Contribution. While you get a $2,000 cradle, the sum isn’t charge deductible.

It’s memorable’s essential that your immediate contributions to a RRSP are just important for what is counted by the Canadian Retirement Agency (CRA). In a given year, the CRA thinks about all contributions to indicated benefits plans (SPP) and pooled enlisted benefits plans (PRPP) toward your yearly total.

To sort out whether or not you’ve over-added to your RRSP, check your CRA account. You ought to get a notification of evaluation that shows you have surpassed the cutoff points and owe charges on the abundance contributions.

In the event that you don’t have the foggiest idea about your contribution limit, check your notification of appraisal charge articulation from your past fiscal year. One more method for registering is by logging with the CRA My Account online entrance.

Need to ascertain it yourself? The cutoff is 18% of your earlier year’s pay with a most extreme cap of $27,830 for 2021.

Penalty for Over-Contributing to an RRSP

Assuming you end up with a RRSP over contribution in abundance of the $2,000 cushion, you might owe charges. The CRA will charge you a 1 percent punishment, surveyed month to month, for every month you’re over the cutoff.

There are ways of limiting your punishment and try not to pay charges on the additional sum. The CRA has a recipe that will assist you with assessing how much expense you owe on your Fix RRSP Over Contribution.

The CRA can drop or postpone the duty on your overabundance contributions assuming that you meet specific prerequisites. The steps beneath will direct you through the cycle for remedying a RRSP over contribution.

How to Fix and RRSP Over Contribution

There are multiple ways of tending to your RRSP over contribution.

- Suffer the consequence

- Pull out the abundance sum

- Show that the contributions were to a passing gathering plan

This is the way every choice works.

Pay the penalty

Prepared to just suffer the consequence? This is the thing you really want to do:

- To start with, you should distinguish the year you made the Fix RRSP Over Contribution by signing into your CRA My Account entryway. Assemble all of your RRSP contribution records for the year in which this happened and every resulting year. These can be found on the notification of appraisal you get from the government subsequent to documenting charges. On the other hand, really look at your computerized assertions from the My Account gateway. Incorporate data about your manager’s contributions to your annuity.

- Get the notification of evaluation the government sent a large number of you recorded charges the earlier year to check your RRSP allowance limit. This data will prove to be useful while ascertaining your RRSP contributions and looking at them against your allowance limits for that year.

- Finish up the T1-OVP, Individual Tax Return for RRSP, PRPP and SPP Excess Contributions return to suffer the 1% duty consequence. Send the finished structure to your assessment community.

If you have any desire to keep away from punishments or charges for late recording, you should pay the expense in 90 days or less. In the event that you don’t suffer the consequence inside the predetermined time-frame, you will bring about additional charges for late recording.

Withdraw the excess amount

The CRA likewise permits you to pull out the overabundance contributions and allure the expense. You should show:

- The abundance contributions were a direct result of an innocent mix-up on your part

- You’re doing whatever it may take to pull out the Fix RRSP Over Contribution

You should compose a letter to the CRA requesting a scratch-off or a waiver of the assessment. This is the thing you want to remember for your letter:

- A conventional solicitation to drop or postpone the assessment

- Duplicates of your RRSP, PRPP, SPP, or enrolled retirement pay store (RRIF) explanations that show when you pulled out the abundance contributions

- Administrative work or documentation that shows your over contribution was a result of a sensible mistake

The withdrawal in pay ought to be incorporated while recording your assessment form. On the off chance that you wanted to guarantee the total measure of your RRSP contribution on your duties good all around without attempting to game the framework, you can guarantee a balancing derivation.

Show that the contributions were to a qualifying group plan

The CRA permits you to extend unused RRSP recompenses from earlier years. This implies that your yearly contribution might surpass the yearly contribution greatest by that sum.

For instance, if you could contribute cash to your RRSP in previous years. Didn’t wind up making use, you can get up to speed. The distinction between what you contributed and the greatest. You were qualified for are added to your ongoing year’s breaking point.

Did your pay go up? This likewise changes your contribution limit cap. Cash moves between annuity plans don’t represent a mark against your limit; contributions to PRPPs and SPPs do.

The Bottom Line

If you find you have made an Fix RRSP Over Contribution. The best thing you can do is take immediate steps to correct it. Keep tabs on your CRA My Account online portal and check your contributions. Against the maximum allowed for the current year.

You can appeal with the CRA to waive the tax if you made an honest mistake. They will review each case of over contribution and consider cancelling or waiving the tax. Up to the day you get your certification from the CRA.